The Verdict

Holding concentrated wealth in a single asset is defensible only when your diversified holdings alone can already fund your retirement to age 90. If a single position represents more than 30% of your investable assets, or is also your primary income source, the risk is almost never compensated. Diversifying, even at a tax cost, is usually the right move.

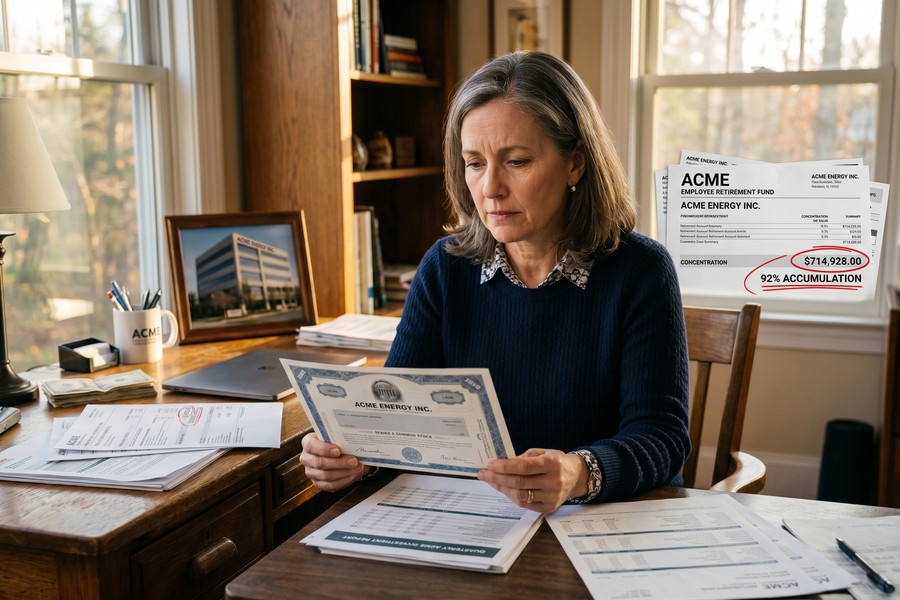

A colleague of mine once described watching his father hold a single telecom stock through a 70% decline because selling “felt like giving up.” The position had been a windfall from an employee stock purchase plan, and over a decade of not trimming it, the family’s net worth became essentially one ticker symbol. That is how concentrated wealth in a single asset usually forms: not through recklessness, but through a combination of discipline, loyalty, and inertia. The factor that swings the decision to diversify is almost always the same one, whether that position has grown large enough that one bad year would permanently alter your financial life. Research cited by the Journal of Accountancy in 2026 found that between 1987 and 2023, 43% of individual stocks in the Russell 3000 suffered a catastrophic loss of 50% or more that was never recovered.

That number matters more now because equity compensation, employer-sponsored retirement plans, and years of asset appreciation have quietly pushed millions of ordinary workers into concentration they did not choose. This is no longer just an executive problem.

| Factor | Reasons to Diversify | Reasons to Hold the Concentrated Position |

|---|---|---|

| Return math | Company-specific risk earns no statistical premium over market risk, extra volatility, no extra compensation | If you hold a genuine outlier, concentration early in a company’s growth phase has historically produced outsized gains |

| Historical base rates | Two-thirds of Russell 3000 stocks underperformed the index over their lifetimes; only 4% of stocks drove all net U.S. market gains since 1926 | You may have strong insider knowledge of the business that the general market has not yet priced in |

| Income dependence | If the asset is also your employer, a single event destroys both paycheck and portfolio simultaneously (the Enron scenario) | Position is small relative to total net worth, so income risk and investment risk are truly separate |

| Tax cost | Gradual, structured diversification spreads the tax bill across years and can use offsets to reduce total liability | A large embedded gain creates a real and immediate tax cost that a lump-sum sale would crystallize all at once |

| Time horizon | Within five years of retirement or a major goal, a sharp drawdown in a single position is often unrecoverable | Long time horizon (20+ years) gives more runway to recover from a drawdown if the business fundamentals are intact |

| Legal constraints | Lock-up periods end; planning for post-lock-up diversification can begin well in advance | Lock-up agreements or SEC Rule 144 restrictions may legally prevent selling for a defined period |

Key Takeaways

- Your single position represents more than 30% of your total investable assets, the threshold most fee-only planners flag as a dominant planning issue

- The same asset is also your primary employer, meaning a layoff and a portfolio crash could hit at the exact same moment

- You are within five years of retirement, a major purchase, or a financial goal that depends on this capital being intact

- You have not run the numbers on what a 50% drawdown in this position would do to your household budget and retirement timeline

- Your emotional reaction to the position’s daily price moves is affecting your sleep, your decisions at work, or your relationship with money

- You have no written plan for when or how you would reduce this position, “I’ll sell when the time is right” does not count as a plan

- Your diversified assets alone could not sustain your lifestyle to age 90 if this position went to zero tomorrow

How Most People End Up With a Concentrated Position

Concentration is rarely a deliberate all-in bet. It usually accumulates quietly. Three origin stories cover the vast majority of cases: employer stock that grew inside a 401(k) or through an ESPP until it dwarfed every other holding; an early investment in a high-growth company that was never trimmed because “why sell a winner”; and an inherited legacy position where the emotional weight of the bequest makes selling feel like a betrayal of the person who left it.

Each origin matters because it shapes the exit options. An ESPP participant typically has ordinary income tax embedded in the position, while an inherited stock usually carries a stepped-up cost basis that dramatically reduces the capital gains exposure, sometimes making a full liquidation nearly tax-free. An early investor holding appreciated shares faces a different math entirely. Diagnosing which situation you are in before reaching for a strategy is the first, most important step.

Most planners treat anything above 10–20% in a single position as a yellow flag and anything above 30% as a dominant planning issue requiring an explicit strategy. If you are also an employee at the same company, some advisors apply an even lower threshold, because your human capital (your future wages) is itself a form of exposure to that company’s performance. Platforms like Fidelity Investments and Vanguard both publish guidance framing an employee’s future wages as a correlated exposure to their employer’s stock, which is why financial planners treat the combined figure, not just the portfolio percentage, as the relevant risk number. Understanding how equity compensation fits into the full picture is worth reviewing; we covered the mechanics in detail in our piece on RSUs and stock options in a wealth-building plan.

The Double-Exposure Trap That Most Advice Ignores

When both your paycheck and your portfolio depend on the same company, one adverse event can destroy both simultaneously. This is the single most underappreciated dimension of concentration risk, and it gets almost no attention in articles aimed at ordinary employees rather than executives.

The Enron bankruptcy in 2001 is the cleanest case study. Thousands of employees held company stock in their 401(k) plans, in some cases it was the majority of their retirement savings, and when Enron collapsed, they lost their jobs, their retirement accounts, and in many cases their health insurance in a single moment. Enron is often framed as a fraud story, which it is, but the financial catastrophe for employees was a concentration story. The fraud could only devastate them because there was no diversification to absorb the blow.

That same structural trap exists today for millions of mid-career workers. FINRA’s investor guidance on concentration risk is direct on this point: holding the majority of your financial assets in a single stock creates outsized exposure to loss, and simply holding funds rather than individual shares does not automatically protect you if those funds are heavily weighted toward your employer’s sector. Boeing fell from above $350 to around $95 in 2020 and had still not recovered to its pre-pandemic peak years later; employees who held Boeing stock in their retirement accounts while also working for the company absorbed that drawdown on both fronts at once.

Fidelity Investments has published guidance noting that when a stock or sector experiences a significant decline, a portfolio concentrated in that single name may suffer far greater volatility than a diversified asset mix would. The practical implication is straightforward: the diversification benefit that an S&P 500 index fund provides by spreading exposure across hundreds of companies is entirely absent when a single ticker dominates your holdings.

For near-retirees, this double exposure problem becomes acutely dangerous because of sequence-of-returns risk. A sharp decline in a concentrated position in the two to three years before or after retirement can permanently impair a portfolio in a way that a diversified drawdown usually cannot. There is no decades-long recovery runway left. If you are within five years of stopping work, the single-asset question is among the most urgent financial decisions on your plate. Our piece on bond allocation in retirement portfolios addresses this transition period in depth.

Why the Bigger the Gain, the Harder It Is to Sell

The psychological barrier to diversifying grows in direct proportion to the size of the unrealized gain, which means risk compounds precisely as the problem becomes most dangerous. Three behavioral forces drive this: overconfidence (treating past performance of a specific stock as evidence of your own judgment), status quo bias (inaction feels neutral even when inaction is an active choice to maintain risk), and loss aversion anchored to a peak price rather than the current one.

The embedded gain itself functions as a lock-in mechanism. A position worth $2 million with a $200,000 cost basis carries $1.8 million in unrealized gains. Selling triggers a tax event that feels like a loss, even though no economic loss has occurred, you are simply converting paper wealth to actual wealth at a cost. The bigger that number, the more painful the trigger feels, and the more rational the brain makes inaction sound.

There is also an identity dimension that financial planners rarely discuss openly. Founders, executives, and long-tenured employees frequently feel that trimming a concentrated position is a statement of doubt about the company, a small betrayal. This is not irrational; conviction and loyalty are part of how concentrated positions are built. But the role of investor and the role of employee require different reasoning. Holding the stock because you believe in the company is a reasonable investment thesis. Holding it because selling feels disloyal is a psychological trap dressed up as a conviction.

SEC Commissioner Mark T. Uyeda has stated plainly that diversification is not a theoretical construct but “a widely accepted foundational principle of sound investing” that is “the mechanism by which investors can reduce exposure to any single asset or market event.” Knowing this intellectually is easy. Acting on it when there is $1.8 million in gains sitting there is something else entirely.

The Tax Problem Is Real, and Often Overstated as a Reason to Do Nothing

Yes, the tax bill on a large concentrated position is significant. A $5 million position with a $1 million cost basis carries $4 million in embedded capital gains. At the current federal long-term capital gains rate of 20%, plus the 3.8% Net Investment Income Tax under the Affordable Care Act, a full immediate liquidation could generate a federal tax liability exceeding $800,000 before state taxes. That number is real. It is also not a reason to do nothing.

The most expensive mistake planners see is conflating tax deferral with tax elimination. Holding the position does not make the tax go away; it delays it while concentration risk continues to accumulate. Meanwhile, the position could decline, and a 40% drop on a $5 million position is a $2 million loss that no future tax saving can offset. The cost of inaction, in that scenario, is far larger than the tax bill would have been.

Structured diversification over three to five years changes the math materially. Staged selling across multiple tax years keeps capital gains within lower brackets. Contributing appreciated shares directly to a Donor Advised Fund eliminates capital gains entirely on the donated amount while generating a charitable deduction. Direct indexing through a separately managed account, a service now offered by firms including Fidelity Investments, Charles Schwab, and Vanguard through their respective managed account programs, can harvest losses elsewhere in the portfolio to offset gains from the sale. Some fintech platforms, including SoFi and Betterment, have also introduced lower-minimum direct indexing products aimed at investors who do not yet meet the higher asset thresholds traditional wealth managers require. These strategies do not eliminate the tax cost, but they can reduce it substantially while the concentration risk decreases each year the plan is in motion.

FINRA’s guidance on asset allocation and diversification is unambiguous: allocating 100 percent of assets into a single security or asset class exposes investors to concentration risk, and diversification is the mechanism for reducing that exposure. The tax conversation belongs inside that framework, not as an argument against diversifying at all.

One honest concession is worth making here. Gradual selling alone can take ten or more years to meaningfully reduce a very large position, and more complex strategies like exchange funds or long/short overlay structures add counterparty complexity and management fees that erode part of the benefit. These are not perfect tools. They are better tools than holding an undiversified position indefinitely, but anyone who tells you there is a fully painless exit from a large concentrated position is selling something.

Who Should and Who Should Not Diversify Aggressively

Good candidates

Diversification is most urgent for people whose financial security genuinely depends on this position behaving well.

- An employee with more than 20% of their retirement account in their employer’s stock, especially if that employer also provides their health insurance and their primary income

- A near-retiree within five years of leaving work whose lifestyle budget depends on the concentrated position remaining intact

- An executor or heir who inherited a low-basis position in a sector they have no expertise in, and who is holding it primarily because selling feels like a statement

- A small business owner whose personal net worth is more than half tied up in the business itself, a non-stock asset concentration that is just as dangerous and far less discussed; if you are building wealth outside a traditional employer structure, the principles in our guide on wealth building beyond a 9-to-5 apply directly here

- Anyone who catches themselves checking this one position’s daily price move more than once a day, because that anxiety is telling you something accurate about your risk exposure

Who should skip aggressive diversification (for now)

There are genuine cases where holding is reasonable, at least temporarily.

- A founder inside an active lock-up period who is legally restricted from selling, the right move is planning for post-lock-up diversification now, not wishing away a legal constraint

- An investor whose concentrated position is below 10% of total investable assets, where the single-asset risk is truly negligible relative to the overall portfolio

- Someone whose diversified assets alone, excluding the concentrated position entirely, can already sustain their lifestyle through age 90 with room to spare, and for whom the position zeroing out tomorrow would be an annoyance rather than a catastrophe

- A long-horizon investor (20+ years to a major goal) in the early stages of building a position in a company they have genuine analytical reasons to believe in, where the position is not yet dominant in the portfolio

Frequently Asked Questions

How much of my portfolio is too much to have in one stock?

Most fee-only financial planners treat 10–20% in a single position as a yellow flag and anything above 30% as a concentration problem requiring an explicit strategy. If that position is also your employer, some advisors apply an even lower threshold because your future wages are themselves a form of exposure to the same company.

Is concentration risk only a problem with stocks?

No. A primary residence plus a rental property that together represent 80% of a household’s net worth creates the same structural vulnerability as a concentrated stock position. A small business that is also the owner’s sole income source is another form of single-asset concentration. The equity-specific framing misses a large share of people who have this problem in real estate or private business ownership.

Does it make sense to hold a concentrated stock position until death to get the step-up in cost basis?

Some holders implicitly rely on this strategy, and it is legally legitimate under current law; heirs receive a stepped-up basis that eliminates the embedded capital gains at death. The policy risk is real, though: this provision has been the target of proposed legislative changes more than once, and depending on a tax rule that could be modified before you die is a fragile planning assumption. For most people, the decades of uncompensated concentration risk is not a reasonable price for the tax benefit.

What is the cheapest way to reduce a concentrated stock position?

Staged selling spread across multiple tax years, sometimes called bracket management, is the most straightforward and least expensive approach. Pairing it with direct indexing to harvest offsetting losses reduces the net tax cost further. Contributing appreciated shares directly to a Donor Advised Fund eliminates capital gains entirely on the donated amount, which is particularly efficient for investors who already give to charity.

Can I use a concentrated position in my 401(k) to diversify tax-free?

Inside a 401(k), you can reallocate among available funds without triggering a taxable event, which makes employer stock concentration inside a retirement account one of the easiest and lowest-cost versions of this problem to fix. The main practical barrier is that some employer plans restrict the frequency of reallocation transactions, but this is generally addressable. The FDIC and the Department of Labor both publish investor education materials covering retirement account diversification basics, and the SEC’s guide on asset allocation and diversification covers the underlying principles clearly for retirement account holders.

Is it worth paying a financial advisor to help with a concentrated position?

For positions above roughly $500,000, the strategies available, direct indexing, exchange funds, layered staged selling, are complex enough that the fee for a fee-only advisor or a tax-aware wealth manager is typically recovered many times over in tax savings and risk reduction. For smaller positions, a one-time consultation with a Certified Financial Planner (CFP) is usually sufficient to build a plan. Understanding when a robo-advisor is enough versus when a human advisor adds value is worth thinking through before you engage anyone.

The broader point is one Seth Klarman, founder and president of the Baupost Group, put plainly: Since we are not able to predict the future, we cannot risk such concentrations.

That framing, not as a regulatory rule but as an acknowledgment of epistemic humility, is probably the most useful way to approach this. Concentration is a bet that you know something others do not, and that the future will cooperate. Diversification is an acknowledgment that neither assumption holds reliably over time. If you are interested in how risk tolerance gets misapplied more broadly in wealth-building decisions, our piece on common mistakes in risk tolerance is worth reading alongside this one.

FINRA has noted that “highly concentrated investments can pose risk, and that risk is heightened when the concentrated investment is a complex product”, a reminder that the problem scales with both concentration and complexity, not just one or the other.

Sources

- Journal of Accountancy (AICPA), Ways to De-Risk Concentrated Stock Portfolios

- Herbein Financial Group, Why Most Stocks Underperform and What to Do About It (citing Bessembinder, 2018)

- FINRA, Investor Guidance: Concentration Risk

- FINRA, Asset Allocation and Diversification

- U.S. Securities and Exchange Commission, Beginner’s Guide to Asset Allocation, Diversification, and Rebalancing

- SEC Commissioner Mark T. Uyeda, Remarks on Diversification Deficit and 401(k) Private Markets Access

- Fidelity Investments, How to Diversify Concentrated Positions