Quick Answer

In the zero based budgeting vs envelope debate, zero-based budgeting wins for detail-oriented planners who need full income control, while the envelope method works better for overspenders targeting specific categories. As of July 2025, studies show envelope-style spending reduces impulse purchases by up to 30%, while zero-based budgeting users report saving an average of $200 more per month than those with no structured budget.

The zero based budgeting vs envelope method debate comes down to one core difference: how you assign every dollar. Zero-based budgeting, popularized by personal finance author Dave Ramsey and corporate strategist Peter Pyhrr, requires your income minus expenses to equal zero each month. According to NerdWallet’s budgeting research, households that track every dollar are twice as likely to meet savings goals as those using informal methods.

With living costs still elevated in 2025, choosing the wrong budgeting system means lost savings, not just inconvenience. The right fit depends on your spending triggers, tech comfort, and how granular you want to get.

What Is Zero-Based Budgeting and How Does It Work?

Zero-based budgeting assigns every dollar of income to a specific category until your budget reaches exactly zero — not zero dollars in your account, but zero unassigned dollars. You start from scratch each month, justifying every expense rather than rolling over last month’s numbers.

The method forces intentional decisions on each spending category: housing, groceries, subscriptions, debt payments, and savings all get a line. Apps like YNAB (You Need A Budget) and EveryDollar (Ramsey Solutions) are built specifically around this framework. YNAB reports that new users save an average of $600 in their first two months by closing spending gaps they didn’t know existed.

Who Benefits Most From Zero-Based Budgeting?

Zero-based budgeting suits people with irregular income the most — gig workers and freelancers who need to re-allocate income every cycle benefit greatly from its reset approach. It also works well for anyone with complex financial goals like debt payoff, investing, and saving simultaneously. If you’re also wondering whether to prioritize debt reduction, our guide on whether to pay off debt or invest first pairs well with this framework.

Key Takeaway: Zero-based budgeting assigns every dollar a job before the month starts. YNAB data shows new users save an average of $600 in their first two months — making it one of the highest-ROI budgeting systems available today.

What Is the Envelope Method and How Does It Work?

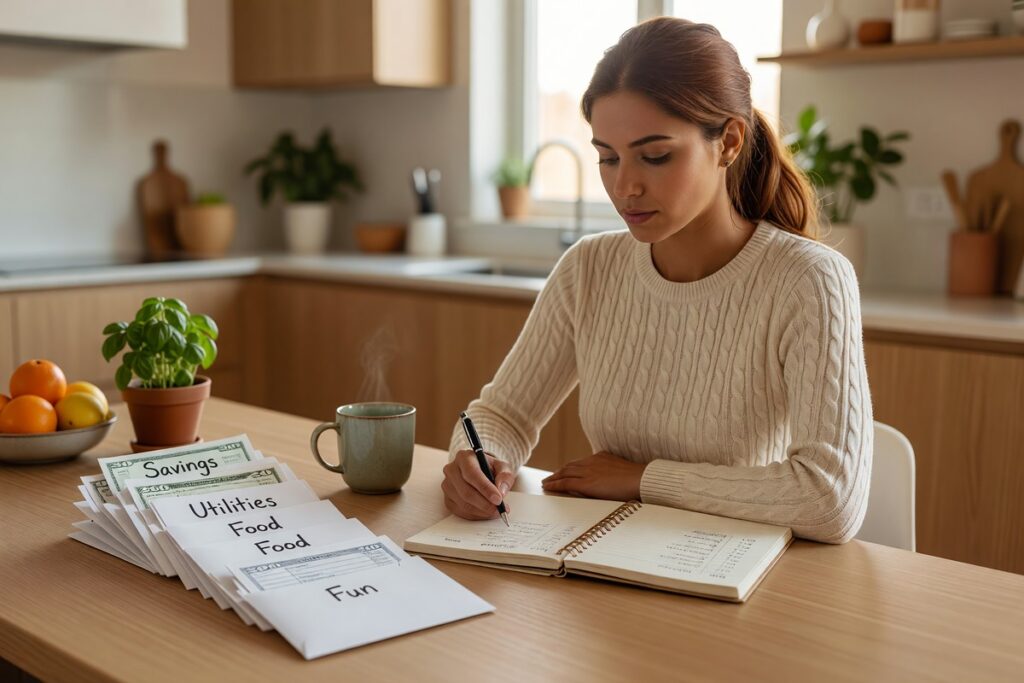

The envelope method divides cash into labeled physical envelopes by spending category — groceries, dining, entertainment, gas — and once an envelope is empty, spending in that category stops for the month. It is one of the oldest personal finance systems, dating back decades before digital banking.

The psychological power is significant. Research cited by the Consumer Financial Protection Bureau (CFPB) confirms that spending physical cash reduces purchase amounts compared to card-based transactions. A widely cited MIT study found consumers spend up to 100% more when paying by credit card versus cash — the tactile friction of handing over bills makes the cost feel real.

Digital Envelope Systems

Apps like Goodbudget and Mvelopes replicate the envelope concept digitally for people who rarely carry cash. These tools let you pre-load virtual envelopes and track spending against each one in real time. Digital envelopes solve the cash-handling burden while preserving the category-limit discipline the original method provides.

Key Takeaway: The envelope method uses category spending limits to prevent overspending. Physical cash usage can cut impulse spending by up to 30% according to behavioral economics research — making it a strong choice for anyone with a history of overspending on discretionary categories. Learn more from the CFPB’s consumer money tools.

How Do These Two Methods Compare Head-to-Head?

In the zero based budgeting vs envelope comparison, the core difference is scope: zero-based budgeting covers your entire financial picture, while the envelope method typically focuses on discretionary spending. Both require intentionality, but they demand different levels of effort and financial literacy.

Zero-based budgeting requires more setup time — typically 30–60 minutes per month to build the plan plus weekly check-ins. The envelope method takes less planning; you withdraw cash, split it, and spend. However, envelopes don’t naturally account for savings goals, investments, or irregular expenses like annual insurance premiums unless you create specific envelopes for them.

| Feature | Zero-Based Budgeting | Envelope Method |

|---|---|---|

| Setup Time | 30–60 min/month | 10–20 min/month |

| Best For | Full financial control | Discretionary overspending |

| Cash Required | No | Yes (or digital app) |

| Savings Integration | Built-in line item | Requires dedicated envelope |

| Irregular Income Fit | Excellent | Moderate |

| Top Tool | YNAB, EveryDollar | Goodbudget, Mvelopes |

| Average Monthly Savings Gain | $200+ | Varies by category discipline |

“The best budget is the one you’ll actually stick to. Zero-based budgeting builds financial awareness across your entire income, but envelope systems win on behavioral compliance for people who struggle with card-based overspending.”

Key Takeaway: Zero-based budgeting covers your full financial picture; the envelope method targets discretionary control. Zero-based users set up budgets in 30–60 minutes monthly, while envelopes take under 20 minutes — making envelopes easier to start but zero-based more comprehensive long term. See how to build wealth on a $40,000 salary using structured budgeting as a foundation.

Which Method Actually Produces Better Results?

Both methods work — but for different problems. Zero-based budgeting consistently outperforms for wealth-building goals. The envelope method outperforms for behavioral spending control. The right choice depends on what is actually breaking your budget.

According to a behavioral economics review published in Annual Review of Economics, the “pain of paying” with cash is a measurable psychological deterrent — which is why envelope users often reduce grocery and dining spend faster than zero-based budgeters using apps. However, zero-based budgeting forces you to plan for savings, retirement contributions, and debt payoff at the category level, which envelopes often ignore. If you’re just starting to think about retirement savings alongside budgeting, see our guide on how to start saving for retirement in your 40s.

When to Combine Both Methods

Many financial planners suggest a hybrid: use zero-based budgeting as the master plan, then apply envelope-style limits to two or three discretionary categories where overspending is habitual. This captures the macro-control of zero-based budgeting and the behavioral friction of envelopes.

The 50/30/20 rule, endorsed by U.S. Senator Elizabeth Warren in her book “All Your Worth,” provides a simpler scaffolding, but both zero-based and envelope methods offer more precision. For households carrying high-interest debt, pairing a structured budget with a debt-versus-investing strategy amplifies results significantly.

Key Takeaway: A hybrid approach — zero-based budgeting for the full plan, envelopes for discretionary categories — delivers the strongest results. Households using structured budgets are twice as likely to hit savings goals according to NerdWallet’s budgeting research compared to unstructured spenders.

How Do You Choose the Right Budgeting Method for Your Situation?

Choose zero-based budgeting if you have multiple financial goals running simultaneously — debt payoff, emergency fund, and investing at the same time. Choose the envelope method if your main problem is one or two spending categories you consistently blow every month.

Your relationship with technology matters too. Zero-based budgeting apps like YNAB cost $14.99 per month (or $99/year), which pays for itself quickly if you close spending gaps. The envelope method costs nothing if you use physical cash, or you can use Goodbudget‘s free tier for digital envelopes. According to the Federal Reserve’s 2023 Report on the Economic Well-Being of U.S. Households, 37% of Americans could not cover a $400 emergency expense — a statistic that makes any structured budgeting method worth the learning curve.

If data privacy is a concern when linking your accounts to budgeting apps, review how open banking alternatives can protect your financial data before connecting any third-party tool.

Key Takeaway: Pick zero-based budgeting for multi-goal financial management; pick envelopes for targeted spending control. With 37% of U.S. adults unable to cover a $400 emergency per the Federal Reserve’s 2023 household survey, adopting either structured method is far better than budgeting informally.

Frequently Asked Questions

Is zero-based budgeting the same as the envelope method?

No. Zero-based budgeting allocates every dollar of income across all categories — including savings, debt, and bills — until income minus expenses equals zero. The envelope method primarily limits spending in specific discretionary categories using cash or virtual envelopes. They share a budgeting mindset but differ in scope and mechanics.

Which budgeting method is better for paying off debt?

Zero-based budgeting is generally better for debt payoff because it forces you to assign a specific dollar amount to debt repayment every month as a line item. The envelope method can support debt payoff if you create a dedicated debt envelope, but it doesn’t naturally enforce the full-income discipline needed to accelerate payoff.

Can I use the envelope method with a debit card instead of cash?

Yes. Apps like Goodbudget and Mvelopes replicate the envelope system digitally, letting you track spending against category limits without using physical cash. The behavioral benefit of cash friction is reduced with digital envelopes, but category discipline is maintained. Many users find digital envelopes a practical compromise.

How long does it take to see results from zero-based budgeting vs envelope?

Most users see measurable results within 60–90 days with either method. YNAB reports new zero-based budgeting users save an average of $600 in their first two months. Envelope users typically see discretionary spending drop within the first month as the visual limit of each envelope creates immediate behavioral change.

Does zero-based budgeting work for irregular income?

Yes, and it is often the preferred method for irregular income earners. You budget based on your lowest expected monthly income and adjust upward when you earn more. This approach, sometimes called income-first or baseline budgeting, prevents lifestyle inflation during high-earning months. Freelancers and gig workers find this particularly effective.

What is the biggest mistake people make with the envelope method?

The most common mistake is not creating envelopes for irregular expenses — annual insurance premiums, car maintenance, and holiday gifts — which leads to budget busts when those costs arrive. A complete envelope system should include sinking fund envelopes for predictable but infrequent expenses. Without them, the method only solves part of the overspending problem.

Sources

- NerdWallet — What Is Zero-Based Budgeting?

- YNAB — How Much Money YNAB Users Save

- Consumer Financial Protection Bureau (CFPB) — Money As You Grow

- Federal Reserve — Report on the Economic Well-Being of U.S. Households (2023)

- Annual Review of Economics — Behavioral Economics of Consumer Finance

- Investopedia — Zero-Based Budgeting Definition and Methodology

- Goodbudget — The Envelope Budgeting Method Explained