Our Take

For most career changers, the standard three-to-six month emergency fund is not enough. The average U.S. job search now runs 22.9 weeks, and career changers, who often start in junior roles or require retraining, commonly face six to twelve months of transition time. Budget for nine to twelve months of bare-minimum expenses plus a separate transition cost fund. The case for the traditional rule holds only if you are making a lateral move within the same field and already have a firm offer in hand before resigning.

Career transitions are more expensive and slower than most people plan for. 27.5% of all unemployed Americans were long-term unemployed in May 2026, according to the Bureau of Labor Statistics Employment Situation report, a number that reflects a hiring market that has measurably slowed since 2021. Employer time-to-fill positions has risen 24% since then, and the average number of interviews per hire has increased 42% according to SHRM benchmarking data. The gap between leaving one income and receiving another is longer, and more costly, than the advice most people carry into a transition.

This article is for employed professionals who are actively planning a career change and want a concrete financial plan before giving notice. The recommendation works when you have lead time to prepare; it gets harder when you are already out of work without a runway.

Key Takeaways

- The average U.S. job search lasts 22.9 weeks, according to BLS data cited by Careerminds, career changers should plan for six to twelve months, not three to six.

- Only 55% of U.S. adults had saved enough to cover three months of expenses, per the Federal Reserve’s 2025 household well-being report, meaning nearly half start a transition already exposed.

- Freelance bridge income carries a 15.3% self-employment tax on net earnings that W-2 employees never see; failing to set aside 25–30% of every payment creates a tax bill most career changers don’t anticipate until April.

- Cashing out a $30,000 401(k) to fund a transition typically nets under $20,000 after the 10% early withdrawal penalty and ordinary income tax, a concrete loss that rolling to an IRA entirely avoids.

- In my observation, the readers who survive the income gap most cleanly are the ones who separated their “survival number” from their current lifestyle spend at least 90 days before resigning, not after the last paycheck clears.

Why the Income Gap Hits Harder Than Most Career Changers Expect

The gap is not simply a paycheck pause. It is a compounding sequence of financial hits that arrive before, during, and after the transition, and most budgeting career change guides address only the middle part.

The Exit Costs Nobody Quantifies

Before you leave, audit what leaving actually costs. Unvested employer 401(k) match contributions are forfeited the moment you resign before the vesting cliff. A common four-year graded schedule means leaving at year two can forfeit 50% or more of the employer’s contributions, easily $2,000 to $8,000 depending on your salary and match rate. Sign-on bonus clawback clauses, which most employees sign and immediately forget, typically require full repayment if you leave within twelve to twenty-four months. Tuition reimbursement programs carry similar repayment triggers. Accrued PTO payout rules vary by state; in states with no required payout, that banked time disappears.

These exit liabilities can add $3,000 to $15,000 or more to the real cost of leaving. Add them to your transition budget before you give notice, not after.

The Psychological Cost of Underestimating the Timeline

Financial stress during a job search accelerates exactly the decisions you want to avoid: accepting the first offer regardless of fit, raiding a retirement account, or carrying a high-interest credit card balance to cover groceries. This is a planning problem, not a willpower problem. The career changers who avoid these traps almost always prepared a specific financial runway in advance, not a vague sense that they had “enough saved.”

What I see in practice: Readers who underestimate the timeline by even two months tend to start negotiating against themselves in final-round interviews. The financial pressure is real and it shows. A longer runway is not a luxury, it is a negotiating asset.

Take a Financial Snapshot Before You Give Notice

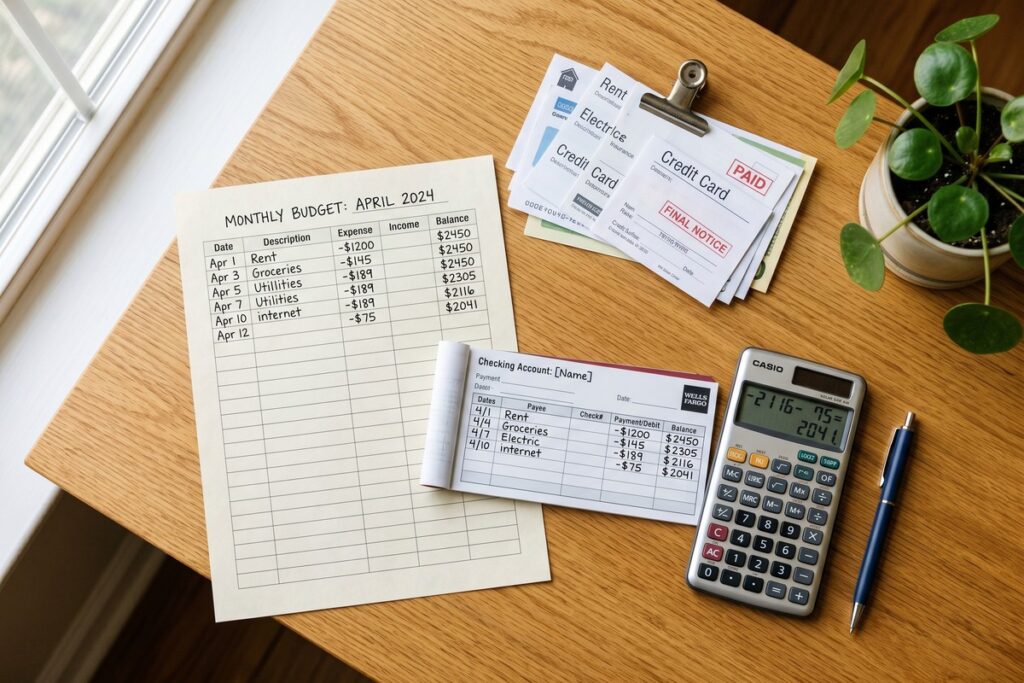

1. Build your bare-bones monthly number. Separate non-negotiable fixed costs, rent or mortgage, utilities, insurance premiums, minimum debt payments, from discretionary spending. This survival number is your actual baseline. It is almost always lower than your current lifestyle spend, and that difference matters when you are calculating how many months of runway you have.

Your Survival Number Formula

Here is the concrete math. Say your bare-bones monthly expenses are $3,200: rent $1,400, utilities $150, groceries $400, insurance $300, minimum debt payments $500, phone and internet $150, transportation $300. Your transition fund target is: ($3,200 × 9 months) + transition costs (certifications, equipment, licensing: estimate $2,500) + healthcare bridge cost (COBRA for an individual typically runs $500 to $700 per month; at $600 for 4 months, that is $2,400). Total: $28,800 + $2,500 + $2,400 = $33,700. That is the savings target for a nine-month runway. Most “save six months” articles would have directed you to hold $19,200, a $14,500 shortfall at the midpoint of a realistic search.

2. Assess debt vulnerability separately. Credit cards and variable-rate debt become destabilizing when income drops. Calculate your minimum monthly debt service obligation as its own line item, independent of living expenses. That number is your hard floor, the amount you cannot fall below without triggering penalty rates, credit score damage, or collection activity.

What clients often miss: The first-paycheck delay at a new job. Even with back-to-back employment, most new hires wait two to four weeks for the first paycheck, and benefit waiting periods, typically 30 to 90 days, mean coverage gaps extend past the income gap itself. Budget a separate allocation for this window specifically.

3. Park the fund correctly. A high-yield savings account or money market fund keeps your transition cash accessible and earning interest. As of mid-2026, many high-yield savings accounts are paying between 4% and 5% APY. A checking account earns nothing; money invested in equities is exposed to drawdown risk at exactly the moment you cannot afford it. If you want guidance on structuring multiple savings buckets without overcomplicating the system, the approach described in our piece on the hybrid budgeting method applies directly here.

What the Six-Month Rule Gets Wrong for Career Changers

The three-to-six month rule was designed for involuntary job loss within the same field, not for a deliberate pivot that may include retraining, a title step-down, and an income reduction that persists after landing the new role.

58% of career changers willingly accept a pay cut to switch fields. Transitions into healthcare, education, and nonprofit roles carry average salary reductions of 10 to 20%. That income dip does not end on the day you start; it extends until you recover seniority in the new field, which research places at 18 to 36 months out. The savings target needs to account for the gap period plus a stabilization buffer, not just the job search itself. Nine to twelve months of bare-minimum expenses, plus a dedicated transition cost fund, is the defensible target for a genuine career change. The exception: if you have a signed offer before resigning and the new role is a lateral or upward move in salary, six months is adequate.

Building a Transition Budget That Works on Variable Income

Ditch the standard monthly budget during the gap. Weekly cash-flow tracking is more effective when income is irregular. Catching an overspend in week two is actionable; discovering it at month-end when rent is already due is not.

The Two-Tier Spending System

Tier one is survival spending: housing, utilities, groceries, insurance, minimum debt payments. These are untouchable and paid first. Tier two is every discretionary dollar, assigned deliberately before the week begins, not tracked after the fact. This structure works because it eliminates the implicit permission that traditional budgets give discretionary spending once fixed costs are covered.

For readers who have found single-system budgets too rigid, the two-tier approach pairs well with a values-based budgeting philosophy, which forces a conscious decision about what discretionary spending actually reflects your priorities during the transition.

Practice Living on the New Salary Before You Quit

Use the BLS Occupational Outlook Handbook and salary aggregators to estimate realistic income in your target role, then run that income through your budget for two to three months while still employed. The delta between your current take-home and the simulated new salary goes directly into the transition fund. This does two things: it builds runway and it tells you whether the new budget is actually livable before you are committed to it.

Where this gets tricky: Bridge income from freelancing looks straightforward until tax season. A career changer earning $3,000 per month freelancing who does not set aside 25–30% for taxes will face a bill of roughly $700 to $900 per month they never budgeted for. Self-employment tax is 15.3% of net earnings, on top of income tax, because freelancers pay both the employee and employer share. Quarterly estimated payments to the IRS are required once you expect to owe $1,000 or more for the year.

One more timing point most guides skip entirely: leaving after a bonus vests, after FSA or HSA funds are fully spent down, or just before a new ACA open enrollment window opens can be worth thousands of dollars in recovered value. These are concrete triggers, not abstract advice about “timing your exit well.” For context on managing healthcare costs specifically during a gap, reviewing your ACA marketplace options when income drops is worth a separate calculation, COBRA premiums for an individual can run $500 to $700 per month, but marketplace subsidies may make an ACA plan significantly cheaper if your projected annual income qualifies.

If subscription and recurring fee management is not already part of your current budget, now is the time. Our breakdown of hidden costs that drain budgets identifies charges most people don’t notice until income forces the issue.

Protecting the 401(k)

Cashing out a retirement account to fund a career change is the most expensive mistake on this list. A $30,000 401(k) balance triggers a 10% early withdrawal penalty ($3,000) plus ordinary income tax. At a 22% federal tax rate, the tax bill is another $6,600, leaving you with roughly $20,400 from a $30,000 balance. Rolling to an IRA or leaving the funds in the former employer’s plan preserves the full amount and costs nothing. The arithmetic makes the decision clear.

| Scenario | Gross Amount | Penalty + Tax (22% bracket) | Net Received |

|---|---|---|---|

| Cash Out 401(k) | $30,000 | $9,600 (10% penalty + 22% income tax) | $20,400 |

| IRA Rollover | $30,000 | $0 | $30,000 |

| Leave in Former Employer Plan | $30,000 | $0 | $30,000 |

Where This Recommendation Falls Short

The strongest case against this approach is the one most readers in financial distress will find immediately: building a nine-to-twelve month transition fund is simply not realistic if you are already living paycheck to paycheck. Bankrate’s 2025 emergency savings survey found that 59% of Americans could not cover an unexpected $1,000 expense from savings. For these readers, the math in this article describes an ideal target, not an immediate one.

The tradeoff is this: a smaller runway is better than no runway. If you can save four months of bare-minimum expenses rather than nine, do that. A four-month cushion with a strict two-tier spending system and active bridge income is survivable. A zero-month cushion is not.

There are also situations where waiting to build a full runway causes real harm. A toxic or unsafe work environment, a layoff that is clearly coming, a physical health issue tied to the job, these are conditions where leaving before the fund is fully built is the right call. The catch is that “I’m unhappy” is different from “this is damaging my health or safety.” Be honest about which category you are in.

The nine-to-twelve month recommendation also assumes you are making a genuine career pivot, changing industries, roles, or required credentials. If you are moving laterally to a competitor in the same field with equivalent or better compensation, the standard six-month emergency fund plus a firm offer in hand is genuinely sufficient. The longer runway is calibrated specifically for the career changer who is starting over in terms of industry relationships, seniority, or credentials.

Finally, this article does not address the post-offer negotiation phase in depth, but that omission has a cost. A sign-on bonus is a direct financial tool for recovering income lost during the search period. Total compensation modeling (health insurance premiums, 401(k) match vesting schedule, remote work cost savings) can make a lower-salary offer financially equivalent to a higher one. Skipping that analysis because you are relieved to have an offer is a real risk. If you need a structured way to evaluate an offer’s full financial picture once it arrives, our guide on budgeting after a job loss covers the reset process in detail.

How We Sourced This

This article draws from the Bureau of Labor Statistics Employment Situation report for May 2026, BLS unemployment duration data for July 2025 as cited by Careerminds, the Federal Reserve’s Report on the Economic Well-Being of U.S. Households in 2024 (published May 2025), and Bankrate’s 2025 emergency savings survey as reported by CBS News. Salary reduction estimates for career-change transitions into healthcare, education, and nonprofit sectors are drawn from occupational wage data available through the BLS Occupational Outlook Handbook. The tax calculation on 401(k) early withdrawals uses the 10% penalty rate codified in IRS Publication 575 and a 22% federal marginal rate, which applies to single filers with taxable income between $47,150 and $100,525 in 2025. All rate and timeline figures reflect data available; readers should verify current high-yield savings APYs and ACA subsidy thresholds independently, as these change frequently.

Frequently Asked Questions

How much money should I save before a career change?

Nine to twelve months of bare-minimum expenses, plus a separate fund for transition costs like certifications, equipment, and healthcare. The standard three-to-six month figure is calibrated for lateral job loss, not a deliberate pivot, career changers face longer search timelines and often take an initial pay cut that extends the financial recovery period.

Should I quit my job before finding a new one during a career change?

Only if you have a full transition fund in place and a clear plan for bridge income. Hiring takes longer than it did pre-pandemic, average time-to-fill has risen to 42 days and the number of interviews per hire has increased 42% since 2021. Resigning without a financial runway under those conditions puts real pressure on your offer-evaluation process.

Can I use freelance work to cover income during a career change?

Yes, but account for the tax cost before you rely on it. Freelance and gig income is subject to 15.3% self-employment tax on top of federal income tax, set aside 25 to 30% of every payment. IRS quarterly estimated payments are required once you expect to owe $1,000 or more for the year; missing them triggers penalties that compound the financial pressure of the transition.

What happens to my 401(k) when I leave my job for a career change?

Roll it to an IRA or leave it in the former employer’s plan, do not cash it out. Cashing out a $30,000 balance at a 22% federal tax rate plus the 10% early withdrawal penalty leaves you with roughly $20,400. The $9,600 loss is permanent and cannot be undone once the distribution is processed.

How do I handle health insurance during the income gap between jobs?

Compare three options before defaulting to COBRA: COBRA continuation coverage (typically $500 to $700 per month for an individual), an ACA marketplace plan (which may be significantly cheaper if your projected income qualifies for subsidies), and a spouse or domestic partner’s employer plan if available. Run the numbers on all three; the cheapest option depends entirely on your projected income for the calendar year.

Sources

- U.S. Bureau of Labor Statistics, The Employment Situation, May 2026

- Careerminds, Average Time to Find a New Job (citing BLS July 2025 data)

- Federal Reserve Board, Report on the Economic Well-Being of U.S. Households in 2024 (May 2025)

- CBS News, Bankrate Emergency Savings Survey 2025

- U.S. Bureau of Labor Statistics, Occupational Outlook Handbook

- IRS Publication 575, Pension and Annuity Income (Early Withdrawal Penalty Rules)

- HealthCare.gov, COBRA Coverage for Unemployed Workers

- IRS, Self-Employment Tax (Social Security and Medicare)